Commercial real estate is a complex and nuanced industry. There are several fallacies that can lead to inaccurate or misleading valuations. This article will shed light on seven of them. Understanding and avoiding these most common pitfalls ensures that your commercial real estate investments are based on accurate and reliable data, leading to better returns and more successful outcomes.

Fallacy 1: Commercial Real Estate Value Is Determined by the Price

Commercial real estate (CRE) is a unique market that requires a different valuation approach than other forms of real estate, such as residential property. Apartments, for example, are typically owner-used, so the only performance indicator of this market segment is the property’s price. Apartment or house value is largely determined by the price at which it can be sold. Hence, many investors, especially newcomers, naturally approach commercial real estate the same. That often leads to faulty valuations since commercial real estate performance is primarily driven by the rent income generated by the property, not the price.

This is because commercial real estate is typically used for business purposes, such as offices, retail spaces, and industrial properties, and generates income through rent payments from tenants. As a result, commercial real estate performance is closely tied to the economy’s strength and the demand for commercial space.

You will make more informed and reliable investment decisions by focusing on the cash flow generated by the property rather than short-term fluctuations in its market value.

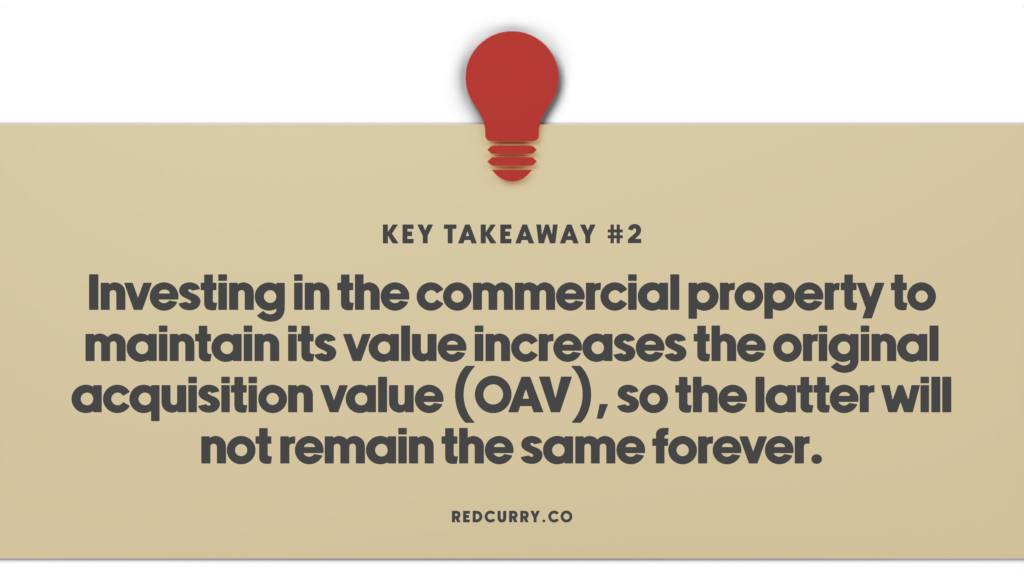

Fallacy 2: Original Acquisition Value Remains Fixed Forever

It is natural to think that the original acquisition value (OAV) remains the same forever. After all, it is the value you bought the property. Reality is slightly different. To maintain the value of a commercial property, one must also invest, and therefore the OAV will not remain unchanged.

Over a period of 10-20 years, a commercial property will require investments of 10-20% of its OAV, primarily to replace heating or cooling systems. This means that over the long term, the OAV of the property will always increase.

In simpler terms, the value of a commercial property will increase over time as long as it is maintained properly. This value comes from the money earned from rent and invested back into the property, not from changes in the property’s market price. The value of the property will always be compared to its original cost, but the focus should be on generating cash flow to increase its value in the long run.

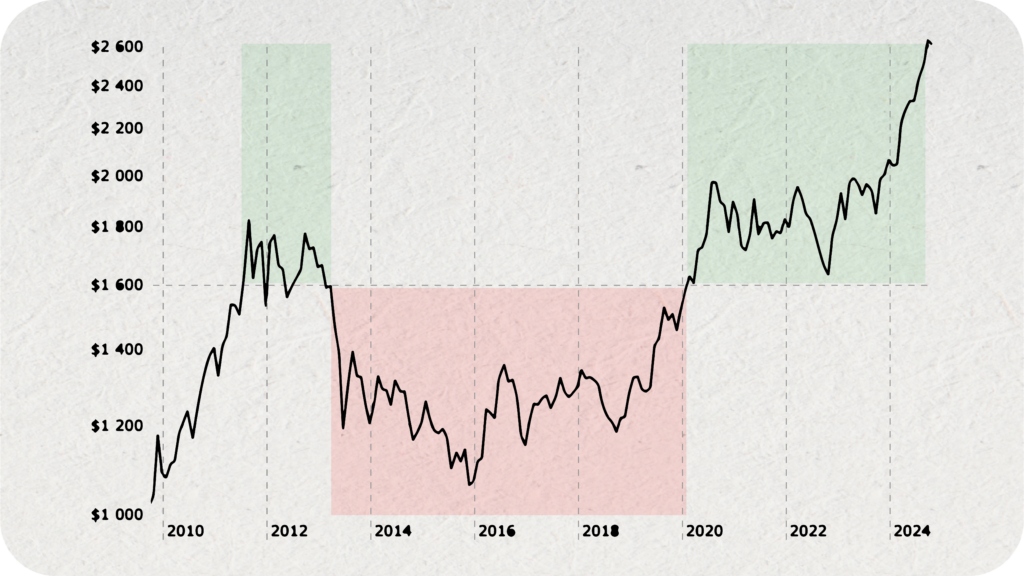

Fallacy 3: Inflation Depreciates CRE Value

Contrary to widespread belief, high inflation rates do not negatively affect the value of the high-quality commercial real estate. In fact, the value of grade A cash-flow-proven properties tends to increase along with interest rates.

As previously mentioned, commercial real estate performance comes primarily from the revenue generated by the property, which is typically tied to an inflation index such as the HCPI (Harmonized Consumer Price Index) published by Eurostat in Europe. Thus, in times of inflation, the income generated by commercial real estate will also increase. In turn, this increased rental income will lead to a higher market value for the property. This means, during times of inflation, the value of commercial properties will tend to rise, making commercial real estate a shield against loss of value caused by inflation.

Fallacy 4: A Property’s Historical Performance is a Good Predictor of Future Performance

Focusing solely on a commercial property’s historical performance is a common mistake in commercial real estate valuation, despite being paraded practically in every investment-related disclaimer. While a property’s past performance can provide valuable insights into its value, it may not necessarily predict how the property will perform in the future.

This is because market conditions can change over time and affect the property’s performance. For example, a property that has historically performed well in a strong market may struggle in a weaker market or vice versa. In addition, changes in the local economy, regulatory environment, or tenant base can also impact the property’s performance.

Therefore, it is essential to take a forward-looking approach when appraising commercial real estate. This involves considering current market conditions and trends that may impact the property’s value. This can also include analyzing demographic trends, market supply and demand, and macroeconomic factors like interest rates and inflation.

Fallacy 5: Underperforming Property Is Due For a Rebound

This is also called the Gambler’s fallacy. It refers to a cognitive bias where individuals assume that past events or outcomes can affect the probability of future events or outcomes, even when the two are not related.

In the context of commercial real estate valuation, this fallacy occurs when an appraiser or investor assumes that a property that has underperformed in the past is more likely to perform well in the future simply because it has underperformed in the past. This assumption is based on the idea that the property is “due for a rebound” or “overdue for a good year” rather than carefully evaluating its current market conditions, trends, and factors that could impact its future performance.

Relying on the belief that a property will perform better in the future simply because it has not performed as well as it should have so far can lead to inaccurate valuations and investment decisions, causing you many problems down the road.

Fallacy 6: Factoring in the Money Spent on the Property

When appraising a property, many new investors automatically factor in the money or effort spent on that property. Even if the investment is unlikely to generate future returns. This is called the sunk cost fallacy. In commercial real estate, this fallacy can be observed when investors or property owners take into account the cost of renovations or upgrades when assessing the current value of the property.

This can be problematic because the cost of previous investments may not necessarily reflect the property’s current market value, particularly if market conditions have changed. The value of a commercial property is determined by a range of factors, including location, market demand, and the property’s potential to generate income.

Be mindful, and don’t let the sunk cost fallacy influence your decisions. Instead, focus on current market conditions and the property’s potential for future growth and income.

Fallacy 7: I Can Do it Myself

While it is certainly possible for an investor to manage their investment on their own, it is important to recognize the many complexities involved in commercial real estate investment.

Successful commercial real estate investment requires financial knowledge and expertise in real estate law, property management, tenant relations, market trends and analysis, and many other specialized fields. Many investors may lack the time, knowledge, or experience to manage all of these aspects effectively on their own.

Working with experienced professionals can help you avoid costly mistakes, navigate complex legal issues, and access market insights that would otherwise be difficult to obtain. Not to mention, experienced professionals can often provide valuable support and expertise.

Redcurry’s Approach to CRE Investments: 5 Tips To Avoid Common Pitfalls of Commercial Real Estate ValuationRedcurry’s Approach to CRE Investments: 5 Tips To Avoid Common Pitfalls of Commercial Real Estate Valuation

1. Focus on cash flow: Ignore short-term fluctuations in market value. Instead, focus on cash flow from rental income. Also, if you can increase the rental income of the property you plan to invest in, you will increase the property’s net asset value (NAV).

2. Focus on market conditions: Ensure that your analysis takes into account current market conditions and trends, as these can significantly impact a property’s value.

3. Examine money spent on a property objectively: Analyze carefully the money and effort that has already been invested in a particular property, as this investment may not generate future returns.

4. Remain unbiased: More often than not, investors seek out information that confirms their preconceived notions about the property while ignoring contradictory information. This is called confirmation bias. It is closely related to anchoring bias, where investors rely too heavily on the first piece of information they receive. Avoid that by seeking out information contradicting your preconceived notions and evaluating it objectively.

5. Bring in outside experts: Consult with experienced professionals, such as appraisers, brokers, and property managers, to get a comprehensive and objective perspective on the property’s value.

Redcurry’s Approach to CRE Investments: 5 Tips To Avoid Common Pitfalls of Commercial Real Estate ValuationFurther Reading

Cannon, Susanne and Col, Rebel A. (2011): How accurate are commercial-real-estate appraisals? Evidence from 25 years of NCREIF sales data. Forthcoming in: Journal of Portfolio Management

Gross, M. (2022). Beautiful cycles: A theory and a model implying a curious role for interest. Economic Modelling, Volume 106.

Clayton, Jim & Ling, David & Naranjo, Andy. (2009). Commercial Real Estate Valuation: Fundamentals Versus Investor Sentiment. The Journal of Real Estate Finance and Economics. 38.

Morri, Giacomo & Benedetto, Paolo. (2019). Commercial Property Valuation: Methods and Case studies. 10.1002/9781119512141.

Wolverton, M. L and Gallimore, P. (1999). Client Feedback and the Role of the Appraiser. Journal of Real Estate Research. 18 (3), 415-432.