For decades, gold has been seen as the ultimate safe haven. When markets crash or inflation spikes, investors turn to the yellow metal as a timeless store of value.

But the world has changed. And while gold’s reputation has endured, the data behind it tells a more complicated story.

The question is no longer “Should you buy gold to protect against inflation?”

The question is “Does gold even do what we think it does?”

This article takes a hard look at the numbers, the myths, and the modern economic reality; because what used to work doesn’t automatically hold up in today’s world. And in a time when value itself is under pressure, it’s worth rethinking what we actually trust to hold it.

The Myth of Gold as a Hedge

Gold has always carried more than just monetary value. For centuries, it was money itself—used by empires, kings, and entire civilizations to store and signal wealth. Even today, in times of economic crisis, gold is often the first asset people flee to. When currencies weaken or markets collapse, gold rises. At least, that’s the narrative.

The belief that gold protects against inflation is deeply rooted in this legacy. It feels intuitive: gold is scarce, physical, and independent of central banks. It doesn’t erode like fiat currencies printed in excess. It doesn’t rely on earnings or interest rates. It just is.

But that perception isn’t purely rational. In many cultures, gold also holds emotional and symbolic meaning. It’s passed down through generations. It’s worn as jewelry, gifted at weddings, and stored as a form of security. Even when its financial performance doesn’t justify the trust placed in it.

This blend of history, symbolism, and selective memory has cemented gold’s role as the inflation hedge of choice. But how much of that belief still holds true under modern scrutiny?

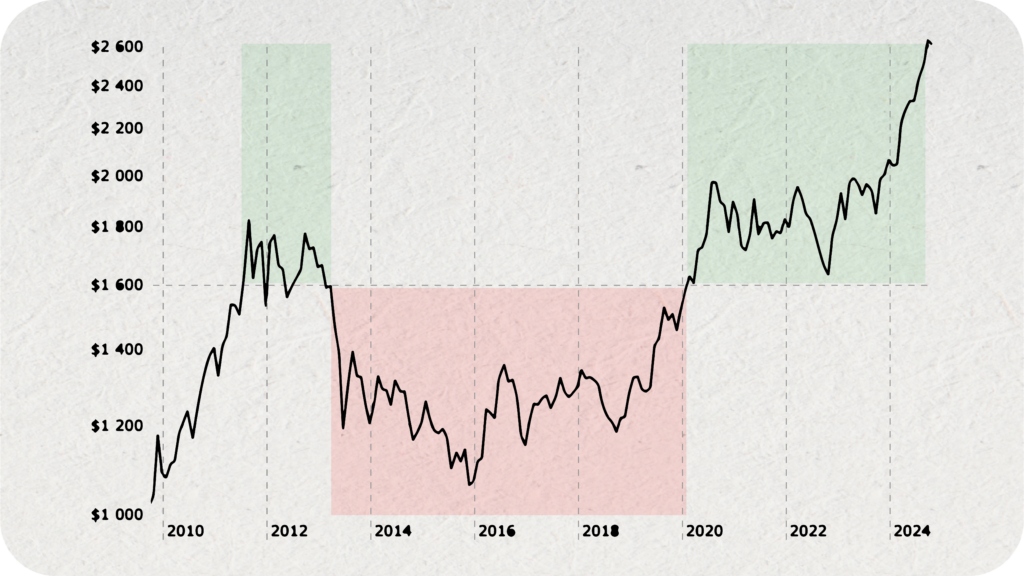

The Data Says Otherwise

For all its mythology, gold’s actual behavior as an inflation hedge is far less reliable than many believe.

Recent studies using the NARDL (Nonlinear Autoregressive Distributed Lag) model (a tool designed to detect complex, asymmetric relationships over time) have cast serious doubt on gold’s consistency. Unlike traditional models, NARDL captures how gold reacts differently to upward versus downward shifts in inflation, offering a more nuanced view of its performance.

What researchers found is telling.

In major economies like the US, UK, and Japan, the relationship between gold and inflation is not only inconsistent, it’s nonlinear. That means gold’s price doesn’t reliably track inflation in a predictable way. Sometimes it moves with inflation. Sometimes it doesn’t. And in many cases, it overreacts to bad news or underreacts entirely.

In countries like France, China, and India, gold fails to act as a long-term hedge at all. Even in places where it shows short-term inflation protection (such as the US or UK) its behavior varies depending on the direction and timing of inflationary pressure.

These findings don’t deny that gold can protect value. But they do undermine the idea that it reliably does so. The comforting narrative of gold as a safe, inflation-proof asset simply doesn’t hold up under close analysis.

Why Gold Falls Short Today

Even if gold carries historical weight and symbolic value, its usefulness as a modern hedge against inflation is limited. And often overstated.

First, gold doesn’t produce income.

Unlike real estate or dividend-yielding assets, gold just sits there. It doesn’t pay interest. It doesn’t grow through reinvestment. Holding it is a passive bet on price appreciation, which makes it less suited for long-term wealth protection; especially in an inflationary environment where purchasing power needs active reinforcement.

Second, it comes with friction.

Physical gold has storage and insurance costs. Digital gold products like ETFs add exposure but lack direct ownership. Liquidity can also become a concern in times of crisis, when everyone is trying to exit at once.

Third, it doesn’t track inflation cleanly.

As the data shows, gold doesn’t rise in a straight line with inflation. It lags, it overshoots, and sometimes it decouples entirely. That makes it unpredictable. Less of a hedge and more of a hope.

And finally, it’s emotionally charged.

Gold has become more myth than model. Much of its demand is driven by sentiment, tradition, or fear. Especially in markets like India and China, where its value is as cultural as it is financial. That makes it less of a rational asset and more of a psychological safety net.

In today’s economy—where inflation is more structural than cyclical, and investors need assets that both protect and perform—gold’s limitations are hard to ignore.

What Makes a Good Inflation Hedge Now?

In a world of persistent inflation and economic uncertainty, the old playbook is no longer enough. Investors today don’t just need assets that feel safe, they need ones that actively work to preserve and grow value.

So what does that look like?

First, it needs to produce income.

An effective hedge isn’t just about holding value. It’s about generating it. Assets that deliver regular, real-world cash flow (like rent, interest, or dividends) naturally counter the effects of inflation by adjusting with the cost of living.

Second, it has to grow with inflation.

Some assets are structurally linked to inflation. For example, real estate with indexed leases or infrastructure projects with inflation-adjusted returns. These built-in mechanisms help the asset’s value and yield rise as prices go up.

Third, it must be accessible and liquid.

A hedge isn’t useful if it’s locked behind legal walls, high entry points, or limited redemption windows. It should be something people can actually use and move when they need to. Not just in theory.

Finally, it should remove the need for market timing.

An inflation hedge should work quietly in the background. If you have to watch charts, guess cycles, or buy the dip, it’s not a hedge. It’s a gamble. Reliability, not volatility, is what protects value over time.

In short, a modern inflation hedge should do more than sit still. It should work—consistently, accessibly, and without constant oversight.

Redcurry: A Modern Alternative

If gold falls short and traditional tools don’t keep up, what comes next?

Redcurry is a digital currency designed with today’s inflation challenges in mind. Instead of relying on sentiment or speculation, it’s backed by something tangible: a portfolio of commercial real estate that generates steady, inflation-indexed rental income.

This real-world income is what powers Redcurry’s gradual value growth. As rent flows in and is used to buy more real estate, the portfolio expands, and Redcurry becomes incrementally more valuable over time. No sudden spikes, no need to time the market. It’s built to deliver steady, compounding growth.

Unlike tokenized real estate or REITs, Redcurry doesn’t require investors to navigate property-specific risks, manage assets, or deal with complex investment vehicles. You don’t need to choose a project, file paperwork, or wait for fund windows to open. You simply hold it—like a currency—and the structure does the work.

In a way, Redcurry aims to do what gold was supposed to do: store value through real economic stress. But it does it by design, not tradition.

Conclusion: Time to Rethink the Safe Haven

Gold will always carry historical weight. Its symbolism is powerful, and its legacy as a store of value is hard to ignore. But when it comes to protecting purchasing power in a modern, inflationary economy, symbolism isn’t enough.

The data is clear: gold’s performance as an inflation hedge is inconsistent, unpredictable, and often dependent on cultural belief as much as economic reality. It may still have a place, but not the one it’s been given by default.

Today’s challenges demand more than tradition. They demand tools that actually perform—assets that produce income, track inflation, and stay usable in the real world.

Redcurry doesn’t try to replace gold’s mythology. It simply offers what gold was supposed to provide: a way to hold value, steadily and reliably, through whatever comes next.

It’s time to question old assumptions. Because the future won’t be secured by what used to work but by what actually does.

Ready to discover how Redcurry can grow your money?

Get started here → Redcurry Pre-Sale